Accounting for biofuels: green, black or shades of grey?

Current controversy

“Biofuel” is a term which covers a range of liquid of gaseous fuels which are produced from organic materials and can be used as alternatives to conventional transport fuels, such as diesel and petrol that are derived from fossil fuels. Since these organic materials, or biomass feedstocks, absorb the same amount of carbon dioxide (CO2) as they release subsequently when the biofuels is burnt, they offer apparent prospects of being “carbon neutral”.

However, the actual benefits of biofuels, as potential means of assisting the mitigation of global climate change, depend on many factors and complex interactions. In particular, it is necessary to determine the total greenhouse gas (GHG) emissions associated with their production and use. In addition to CO2, other GHG emissions, such as methane (CH4) and nitrous oxide (N2O), have to be taken into account.

“Biofuel” is a term which covers a range of liquid of gaseous fuels which are produced from organic materials and can be used as alternatives to conventional transport fuels, such as diesel and petrol that are derived from fossil fuels. Since these organic materials, or biomass feedstocks, absorb the same amount of carbon dioxide (CO2) as they release subsequently when the biofuels is burnt, they offer apparent prospects of being “carbon neutral”.

However, the actual benefits of biofuels, as potential means of assisting the mitigation of global climate change, depend on many factors and complex interactions. In particular, it is necessary to determine the total greenhouse gas (GHG) emissions associated with their production and use. In addition to CO2, other GHG emissions, such as methane (CH4) and nitrous oxide (N2O), have to be taken into account.

Depending on the biomass feedstock and its original source, how and where it is cultivated or otherwise derived, and how it is converted into a biofuels, total GHG emissions can vary from a very low, or, indeed, negative, value to very high values that exceed those from the production and use of conventional transport fuels. Whilst such results have been interpreted in different ways by people with different perspectives, the Biofuels Working Group of the Royal Society concluded that “each biofuels option needs to be assessed individually on its own merits” (Royal Society, 2008).

Life cycle assessment

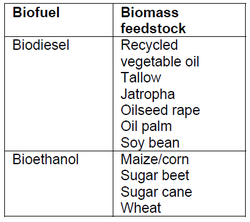

The necessary scientific approach to resolving the current controversy over biofuels involves the application of life cycle assessment (LCA). This established technique consists of evaluating the full process chain of any biofuels, including cultivating, harvesting and transporting or otherwise collecting the biomass feedstock, preparing it for processing by drying or other pre-treatment, converting it to a biofuels and then distributing it to eventual consumers. Examples of current biofuels and their biomass feedstocks are summarised in Table 1.

Life cycle assessment

The necessary scientific approach to resolving the current controversy over biofuels involves the application of life cycle assessment (LCA). This established technique consists of evaluating the full process chain of any biofuels, including cultivating, harvesting and transporting or otherwise collecting the biomass feedstock, preparing it for processing by drying or other pre-treatment, converting it to a biofuels and then distributing it to eventual consumers. Examples of current biofuels and their biomass feedstocks are summarised in Table 1.

|

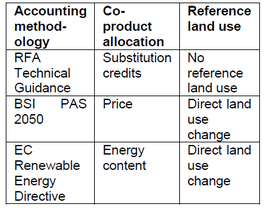

Various considerations throughout the full process chain have to be accommodated and the details of how this is achieved are governed by accounting rules or methodologies. There are a number of different methodologies which are proposed and these have different approaches to two essential aspects of the LCA of biofuels. One aspect concerns “co-product allocation” which determines how GHG emissions are divided between the different outputs that can arise during the production of certain biofuels.

The second aspect addresses “reference land use” which is a means for incorporating the GHG emissions effects of alternative uses of the land for growing biomass feedstocks. At the moment, there are at least three possible methodologies for assessing the total GHG emissions associated with biofuels production. These consist of the Renewable Fuels Agency (RFA) Technical Guidance (RFA, 2008), the British Standards Institution (BSI) PAS 2050 (BSI, 2008), and the European Commission (EC) Draft Renewable Energy Directive (EC, 2008). The differences between these accounting methodologies, with regard to co-product allocation and reference land use, are summarised in Table 2. Methodological effects Differences between accounting methodologies can cause significant differences in estimates of the total GHG emissions associated with biofuels. Relevant and subsequent results have been derived from the Biomass Environmental Assessment Tool (BEAT) which has been produced for the Department for Environment, Food and Rural Affairs (DEFRA) and the Environment Agency in the United Kingdom (DEFRA, 2008). |

Table 1: Current biofuels and

biomass feedstocks

Table 2: Main differences between accounting methodologies

|

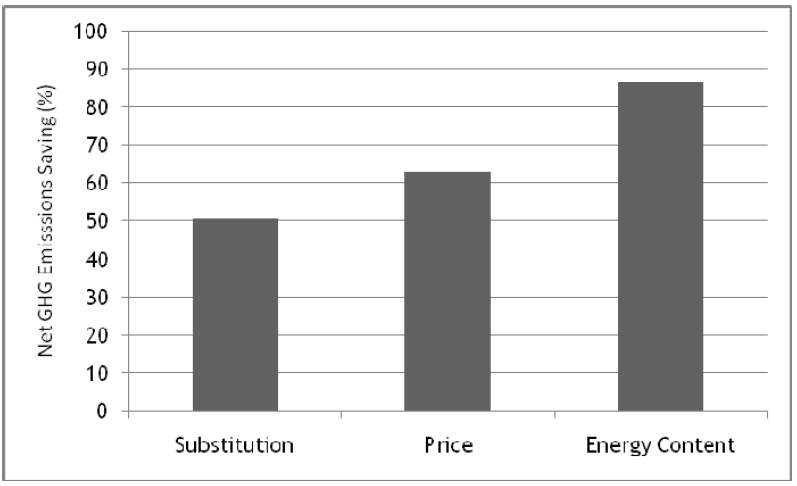

In particular, BEAT has been used to estimate the net GHG emissions savings of biofuels which measures the percentage reduction in total GHG emissions from any given biofuel relative to those of the conventional transport fuel which it replaces. Examples of the effect of applying different co-product allocation procedures to the production of bioethanol from wheat are shown in Figure 1. The main co-product of bioethanol production from wheat is distillers’ dark grains and soluble (DDGS) which is normally sold as animal feed. In this case, using substitution credits which subtract GHG emissions associated with soy meal animal feed that is displaced by DDGS generated the lowest net GHG emissions savings. Whilst co-product allocation by price produces intermediate net GHG emissions savings, using the energy content of the bioethanol and DDGS results in the highest net GHG emissions savings.

Although the current version of the RFA Technical Guidance excludes reference land use, this is being re-considered in the light of the United Kingdom review of the Renewable Transport Fuels Obligation (RTFO). It is possible that all accounting methodologies will be modified to include the effects of direct and indirect land use change (LUC). It is relatively easy to accommodate the GHG emissions effects when alternative land uses do not involve the creation of a useful product such as food.

Although the current version of the RFA Technical Guidance excludes reference land use, this is being re-considered in the light of the United Kingdom review of the Renewable Transport Fuels Obligation (RTFO). It is possible that all accounting methodologies will be modified to include the effects of direct and indirect land use change (LUC). It is relatively easy to accommodate the GHG emissions effects when alternative land uses do not involve the creation of a useful product such as food.

Figure 1: Effect of co-product allocation procedures

on net greenhouse gas emissions savings of

bioethanol production from wheat

|

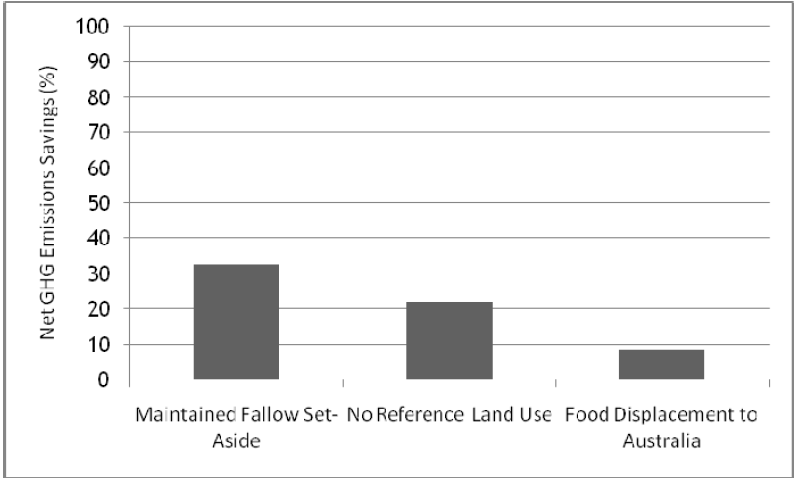

Figure 2: Effect on net GHG emissions savings for

biodiesel production from oilseed rape of reference

land use

|

However, when food or other production is displaced by the cultivation of a biomass feedstock, it is necessary to determine the nature of the displacement and its effects on total GHG emissions. Deciding the location and implications of alternative production is not simple but the consequences for on GHG emissions can be dramatic as shown in Figure 2. This illustrates the effect of net GHG emissions savings for biodiesel production from oilseed rape in the United Kingdom with no reference land use, with cultivation on maintained fallow land and with cultivation on land used to grow oilseed rape for food which is now switched, for example, to Australia (Mortimer, 2006).

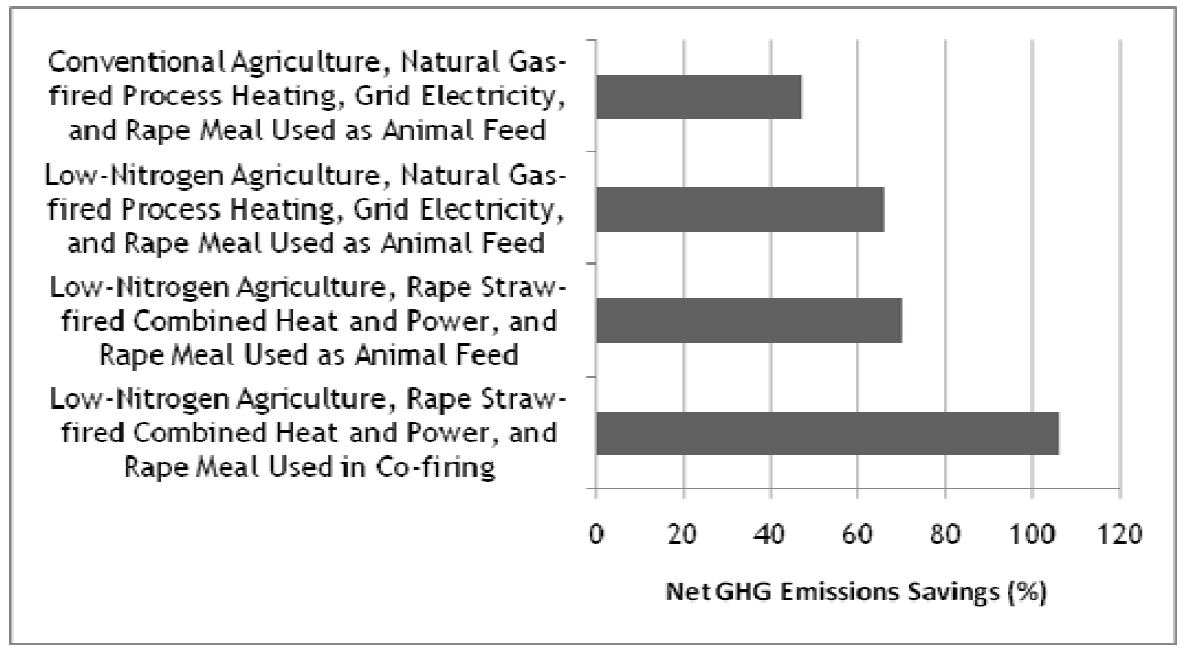

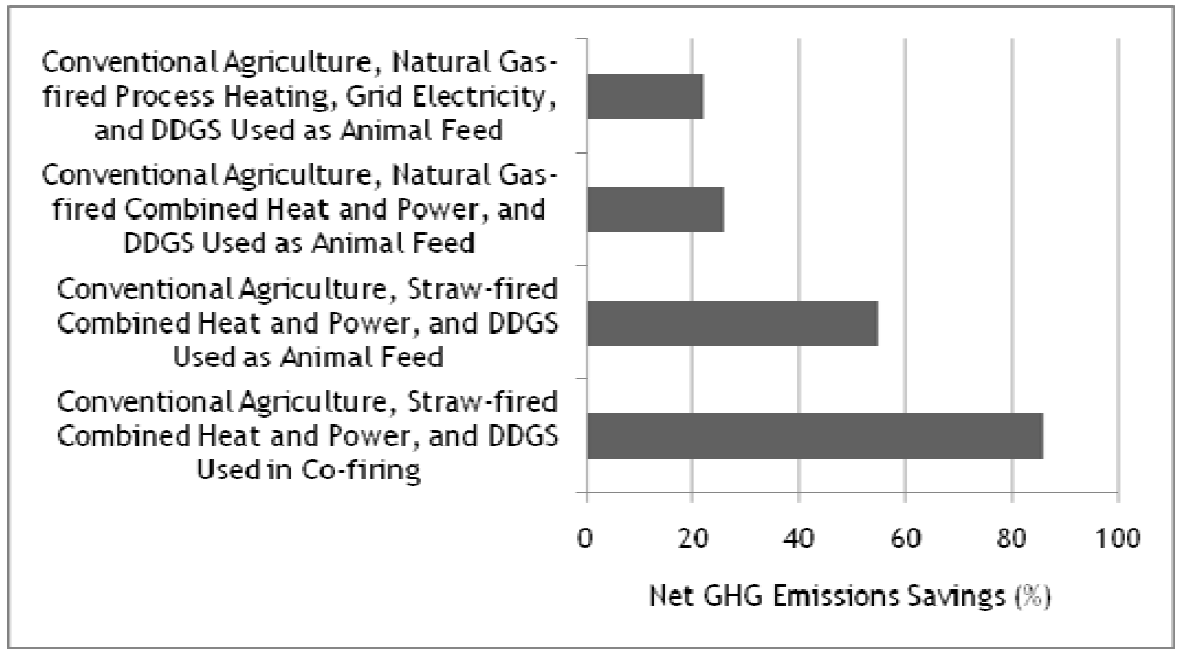

Technological effects

Before considering the important issue of indirect or displaced land use further, it is necessary to address the effects of technological choices on the total GHG emissions of biofuels production. These can have a significant influence on net GHG emissions savings as demonstrated in Figure 3 and Figure 4 for biodiesel production from oilseed rape and bioethanol production from wheat, respectively.

There are many different technological choices in the design of biofuels process chains including different agricultural practices, different means of providing heat and electricity for processing and different uses for the co-products. It can be seen from Figures 3 and 4 that the use of combined heat and power and co-products for fuels can improve net GHG emissions savings substantially.

Technological effects

Before considering the important issue of indirect or displaced land use further, it is necessary to address the effects of technological choices on the total GHG emissions of biofuels production. These can have a significant influence on net GHG emissions savings as demonstrated in Figure 3 and Figure 4 for biodiesel production from oilseed rape and bioethanol production from wheat, respectively.

There are many different technological choices in the design of biofuels process chains including different agricultural practices, different means of providing heat and electricity for processing and different uses for the co-products. It can be seen from Figures 3 and 4 that the use of combined heat and power and co-products for fuels can improve net GHG emissions savings substantially.

Figure 3: Effect of technological choices on net GHG

emissions savings for biodiesel production from

oilseed rape

|

Figure 4: Effect of technological choices on net GHG

emissions savings for bioethanol production from

wheat

|

Displaced land use

The issue of displaced land use is currently the most controversial consideration for biofuels production. The basis of this issue is quite simple. It is possible that biomass feedstocks grown on land for biofuels may displace the cultivation of other crops, especially for food production, into other areas of the world leading to the damage or destruction stocks or sinks of carbon in the soil and vegetation. This could result in the release of substantial quantities of GHG emissions that would equal or exceed the net GHG emissions savings of the original biofuels.

Potentially, this amounts to a powerful case against biofuels production as a means of mitigating global climate change (Fargione et al, 2008; Searchinger et al, 2008). This concern is a major focus of the RTFO review in the United Kingdom. Thorough analysis is required to form robust conclusions and subsequent policy. However, it is clear that the outcomes from any rigorous analysis will always be heavily qualified. In particular, given the existing state of knowledge, it is impossible to be totally confident over the precise and complete chain of land displacement that potentially link the cultivation of any given crop to indirect and remote GHG emissions. Greater understanding which enables this issue to be resolved will only emerge over time. Despite this, broad guidelines can be established. In particular, the destruction of any significant carbon stores, such as continuously grown forest, wetlands, peatlands and permanent grasslands, should be avoided anywhere for any purpose as this is directly responsible, as an act in itself, for global climate change. Hence, emphasis should be placed on growing biomass feedstocks for current biofuels in areas which does not result in land displacement.

The issue of displaced land use is currently the most controversial consideration for biofuels production. The basis of this issue is quite simple. It is possible that biomass feedstocks grown on land for biofuels may displace the cultivation of other crops, especially for food production, into other areas of the world leading to the damage or destruction stocks or sinks of carbon in the soil and vegetation. This could result in the release of substantial quantities of GHG emissions that would equal or exceed the net GHG emissions savings of the original biofuels.

Potentially, this amounts to a powerful case against biofuels production as a means of mitigating global climate change (Fargione et al, 2008; Searchinger et al, 2008). This concern is a major focus of the RTFO review in the United Kingdom. Thorough analysis is required to form robust conclusions and subsequent policy. However, it is clear that the outcomes from any rigorous analysis will always be heavily qualified. In particular, given the existing state of knowledge, it is impossible to be totally confident over the precise and complete chain of land displacement that potentially link the cultivation of any given crop to indirect and remote GHG emissions. Greater understanding which enables this issue to be resolved will only emerge over time. Despite this, broad guidelines can be established. In particular, the destruction of any significant carbon stores, such as continuously grown forest, wetlands, peatlands and permanent grasslands, should be avoided anywhere for any purpose as this is directly responsible, as an act in itself, for global climate change. Hence, emphasis should be placed on growing biomass feedstocks for current biofuels in areas which does not result in land displacement.

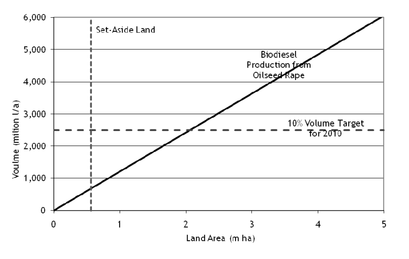

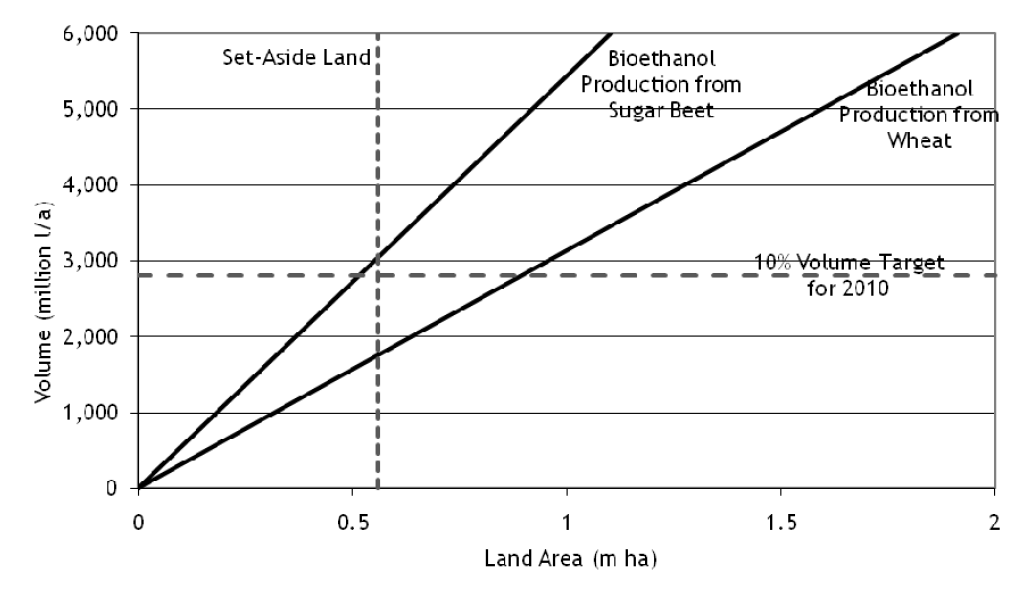

Within the United Kingdom, this would consist of agricultural land, such as set-aside, which is not currently used for productive purposes. This has implications for the total amount of biofuels which can be grown, as suggested by Figures 5 and 6. These indicate the net amount of biodiesel and bioethanol, respectively, that can be obtained from set-aside land in the United Kingdom in comparison with proposed targets for production in 2010. Whilst the existing target cannot be achieved with biodiesel production from oilseed rape, it is more attainable with bioethanol production from wheat and, particularly, sugar beet. This demonstrates that target setting is quite complex and requires qualification to realise real GHG emissions savings. Apart from anything else, the type of biofuels, its biomass feedstock and where this is produced has to be accommodated within essential target-driven policies. As well as avoiding the worst consequences of direct and indirect land use change, the development and commercialisation of future biofuel technologies which may result in very high net GHG emissions savings need to be encouraged.

Figure 5: Potential biodiesel production in the United Kingdom

|

Figure 6: Potential bioethanol production in the United Kingdom

|

Conclusions

A number of important conclusions can be drawn from this brief examination of biofuels. There is a need to harmonise accounting methodologies for the evaluation of total GHG emissions associated with biofuels production and, indeed, all proposed measures for mitigating global climate change to ensure consistency and clarity with results. Such results should form the basis for science-based policies which incorporate targets for net GHG emissions savings. These policies will require sound methods of accreditation for their implementation. Additionally, these policies should promote good technological choices for current biofuels production and encourage the realisation of new biofuels technologies. Above all, land use displacement and the destruction of carbon stores, globally, should be avoided. This is a conclusion which not only affects biofuels production but also has serious implications for the agricultural industry, generally, along with rural and urban development and, ultimately, future human behaviour and lifestyles.

References

British Standards Institution (2008) “PAS 2050 – Specification for the Assessment of Life Cycle Greenhouse Gas Emissions of Goods and Services” Publicly Available Specification, London, United Kingdom.

Department for Environment, Food and Rural Affairs (2008) “Biomass Environmental Assessment Tool, Version 2.0” prepared by AEA Group plc and North Energy Associates Ltd, website launch expected June 2008.

European Commission (2008) “Proposal for a Directive of the European Parliament and of the Council on the Promotion of the Use of Energy from Renewable Sources”, Version 15.4, Commission of the European Communities, Brussels, Belgium.

Fargione, J., Hill, J., Timan, D., Polasky, S., and Hawthorne, P. (2008) “Land Clearing and the Biofuel Carbon Debt” Science Express, www.sciencexpress.org.

Mortimer, N. D. (2006) “The Role of Life Cycle Assessment in Policy and Commercial Development: The Case of Liquid Biofuels in the United Kingdom” 5th Australian Life Cycle Assessment Conference, Melbourne, Australia.

Renewable Fuels Agency (2008) “Carbon and Sustainability Reporting within the Renewable Transport Fuel Obligation” London, United Kingdom.

Royal Society (2008) “Sustainable Biofuels: Prospects and Challenges” London, United Kingdom.

Searchinger, T., Heimlich, R., Houghton, R. A., Fengxia Dong, Elobeid, A., Fabiosa, J., Tokgoz, S., Hayes, D., and Tun-Hsiang Yu (2008) “Use of US Croplands for Biofuels Increases Greenhouse Gases through Emissions from Land Use” Science Express, www.sciencexpress.org.

NIGEL MORTIMER,

North Energy Associates Ltd.,

Watsons Chambers,

5 – 15 Market Place,

Castle Square,

Sheffield S1 2GH,

United Kingdom

Tel: +44 (0) 114 201 2604

E-mail: [email protected]

Biographical details

Nigel Mortimer is one of the founding directors of North Energy Associates Ltd. This consultancy company has been involved in the practical implementation of sustainable energy development since 1991. Nigel has a BSc in Physics and a PhD in Energy Technology. Nigel formerly held the Chair of Sustainable Energy Development at Sheffield Hallam University where he was the Head of the Resources Research Unit. His specific expertise within North Energy includes life cycle assessment. He has managed and undertaken research and consultancy contract work on a broad range of projects in the United Kingdom and elsewhere. His current work involves the evaluation of primary energy inputs and greenhouse gas emissions associated with biomass energy technologies, biomaterials and biochemicals. Clients for this work include the European Commission, the Department for the Environment, Food and Rural Affairs, the Department of Business, Enterprise and Regulatory Reform, the Environment Agency, British Sugar plc, Biofuels Corporation plc and the Northeast Biofuels Consortium. Nigel is a member of the Royal Society’s Biofuels Working Group which recently published “Sustainable Biofuels: Prospects and Challenges.

This article is based on a presentation by Dr Mortimer at the ECG’s 2008 Distinguished Guest Lecture and Symposium ‘The Science of Carbon Trading’.

A number of important conclusions can be drawn from this brief examination of biofuels. There is a need to harmonise accounting methodologies for the evaluation of total GHG emissions associated with biofuels production and, indeed, all proposed measures for mitigating global climate change to ensure consistency and clarity with results. Such results should form the basis for science-based policies which incorporate targets for net GHG emissions savings. These policies will require sound methods of accreditation for their implementation. Additionally, these policies should promote good technological choices for current biofuels production and encourage the realisation of new biofuels technologies. Above all, land use displacement and the destruction of carbon stores, globally, should be avoided. This is a conclusion which not only affects biofuels production but also has serious implications for the agricultural industry, generally, along with rural and urban development and, ultimately, future human behaviour and lifestyles.

References

British Standards Institution (2008) “PAS 2050 – Specification for the Assessment of Life Cycle Greenhouse Gas Emissions of Goods and Services” Publicly Available Specification, London, United Kingdom.

Department for Environment, Food and Rural Affairs (2008) “Biomass Environmental Assessment Tool, Version 2.0” prepared by AEA Group plc and North Energy Associates Ltd, website launch expected June 2008.

European Commission (2008) “Proposal for a Directive of the European Parliament and of the Council on the Promotion of the Use of Energy from Renewable Sources”, Version 15.4, Commission of the European Communities, Brussels, Belgium.

Fargione, J., Hill, J., Timan, D., Polasky, S., and Hawthorne, P. (2008) “Land Clearing and the Biofuel Carbon Debt” Science Express, www.sciencexpress.org.

Mortimer, N. D. (2006) “The Role of Life Cycle Assessment in Policy and Commercial Development: The Case of Liquid Biofuels in the United Kingdom” 5th Australian Life Cycle Assessment Conference, Melbourne, Australia.

Renewable Fuels Agency (2008) “Carbon and Sustainability Reporting within the Renewable Transport Fuel Obligation” London, United Kingdom.

Royal Society (2008) “Sustainable Biofuels: Prospects and Challenges” London, United Kingdom.

Searchinger, T., Heimlich, R., Houghton, R. A., Fengxia Dong, Elobeid, A., Fabiosa, J., Tokgoz, S., Hayes, D., and Tun-Hsiang Yu (2008) “Use of US Croplands for Biofuels Increases Greenhouse Gases through Emissions from Land Use” Science Express, www.sciencexpress.org.

NIGEL MORTIMER,

North Energy Associates Ltd.,

Watsons Chambers,

5 – 15 Market Place,

Castle Square,

Sheffield S1 2GH,

United Kingdom

Tel: +44 (0) 114 201 2604

E-mail: [email protected]

Biographical details

Nigel Mortimer is one of the founding directors of North Energy Associates Ltd. This consultancy company has been involved in the practical implementation of sustainable energy development since 1991. Nigel has a BSc in Physics and a PhD in Energy Technology. Nigel formerly held the Chair of Sustainable Energy Development at Sheffield Hallam University where he was the Head of the Resources Research Unit. His specific expertise within North Energy includes life cycle assessment. He has managed and undertaken research and consultancy contract work on a broad range of projects in the United Kingdom and elsewhere. His current work involves the evaluation of primary energy inputs and greenhouse gas emissions associated with biomass energy technologies, biomaterials and biochemicals. Clients for this work include the European Commission, the Department for the Environment, Food and Rural Affairs, the Department of Business, Enterprise and Regulatory Reform, the Environment Agency, British Sugar plc, Biofuels Corporation plc and the Northeast Biofuels Consortium. Nigel is a member of the Royal Society’s Biofuels Working Group which recently published “Sustainable Biofuels: Prospects and Challenges.

This article is based on a presentation by Dr Mortimer at the ECG’s 2008 Distinguished Guest Lecture and Symposium ‘The Science of Carbon Trading’.

Royal Society of Chemistry Environmental Chemistry Group

Burlington House

Piccadilly London W1J 0BA |

|

© COPYRIGHT 2022. ALL RIGHTS RESERVED.

Website by L Newsome

|