A review of the global supply of rare earths

Prior to the 1990s, rare earth production from the USA, Australia, and India supported global demand, but this changed when lower-cost Chinese supply became available in the mid-1990s. Chinese rare earth production has since dominated supply, accounting for 97% of global production in 2007. Efforts to reduce China's control of the rare earth element industry since the mid-2000s have resulted in intense exploration and development of rare earth element projects and research into recycling rare earth elements used in magnets and phosphors. Chinese dominance of rare earth elements supply is, however, forecast to continue beyond 2020.

The rare earths elements (REEs) include the naturally occurring lanthanide elements, lanthanum through to lutetium, along with yttrium and scandium. Contrary to their name, their combined crustal abundance is in the region of 120 ppm (1), making them more abundant than copper or lead. Individually, however, certain rare earth elements have much lower crustal abundances. For example, lutetium has an average crustal abundance of only 0.2 ppm (1). The rare earths are typically split into two sub-groups: the light rare earth elements (LREEs), which include lanthanum through to samarium (La, Ce, Pr, Nd, Sm), and the heavy rare earth elements (HREEs), which include europium through to yttrium (Eu, Gd, Tb, Dy, Ho, Er, Tm, Yb, Lu, Y). Deposits of REEs occur within primary acidic or late-stage igneous rocks such as carbonatites and alkaline intrusives, or as a result of associated hydrothermal activity. Igneous intrusives may be weathered and leached to form clay mineral deposits enriched in REEs, commonly described as ion absorption clays. Secondary placer deposits of heavy mineral may also be enriched in REEs, and deposits formed by weathering of REE-enriched igneous rocks are mined commercially.

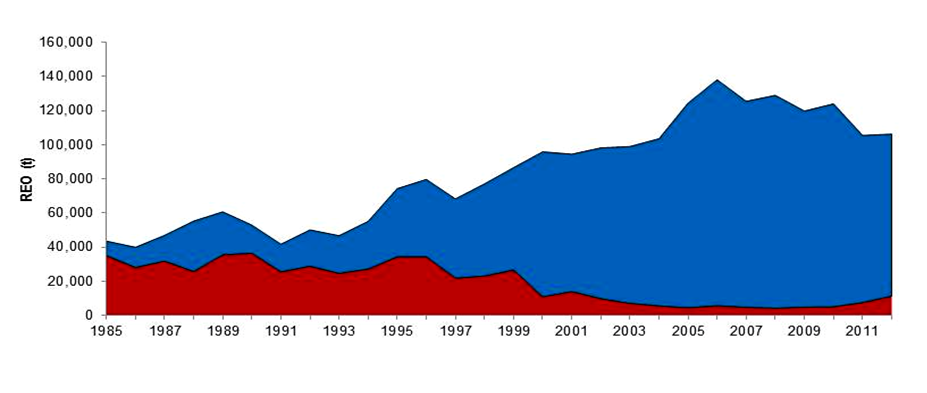

Prior to 1990, the USA was the largest producer of REEs in the world from the Mountain Pass mine, California. Australia, China and India were other major producers of REEs during this period. Between 1990 and 1995, Chinese REE production showed strong growth as a by-product of iron ore mining at the Baiyun Obo deposit in Baotou, Inner Mongolia and production from artisanal and small-scale mines in the southern Chinese provinces. The availability of low-cost REEs from China, combined with the increasing cost of meeting environmental standards, caused miners in Australia, India, and the USA to reduce or close operations, strengthening China’s position (Figure 1).

The rare earths elements (REEs) include the naturally occurring lanthanide elements, lanthanum through to lutetium, along with yttrium and scandium. Contrary to their name, their combined crustal abundance is in the region of 120 ppm (1), making them more abundant than copper or lead. Individually, however, certain rare earth elements have much lower crustal abundances. For example, lutetium has an average crustal abundance of only 0.2 ppm (1). The rare earths are typically split into two sub-groups: the light rare earth elements (LREEs), which include lanthanum through to samarium (La, Ce, Pr, Nd, Sm), and the heavy rare earth elements (HREEs), which include europium through to yttrium (Eu, Gd, Tb, Dy, Ho, Er, Tm, Yb, Lu, Y). Deposits of REEs occur within primary acidic or late-stage igneous rocks such as carbonatites and alkaline intrusives, or as a result of associated hydrothermal activity. Igneous intrusives may be weathered and leached to form clay mineral deposits enriched in REEs, commonly described as ion absorption clays. Secondary placer deposits of heavy mineral may also be enriched in REEs, and deposits formed by weathering of REE-enriched igneous rocks are mined commercially.

Prior to 1990, the USA was the largest producer of REEs in the world from the Mountain Pass mine, California. Australia, China and India were other major producers of REEs during this period. Between 1990 and 1995, Chinese REE production showed strong growth as a by-product of iron ore mining at the Baiyun Obo deposit in Baotou, Inner Mongolia and production from artisanal and small-scale mines in the southern Chinese provinces. The availability of low-cost REEs from China, combined with the increasing cost of meeting environmental standards, caused miners in Australia, India, and the USA to reduce or close operations, strengthening China’s position (Figure 1).

Figure 1: Historical global production of rare earth elements expressed as tonnes of rare earth oxides (REO) (1985-2012). The transition period highlights when China began to increase REE production while non-Chinese producers reduced output or closed their operations. Blue: Production from Chinese sources; Red: Production outside China. Data sourced from Chinese Ministry of Land and Resources, Chinese Ministry of Industry and Information Technology, Chinese National Development and Reform Commission, China Rare Earth Information Centre, Industry/Company reports and Roskill estimates.

Chinese dominance of the REE industry peaked at 97% of global production in 2008, as a sharp drop in demand associated with the global economic downturn led to reduced production from non-Chinese producers. Since 2008, increasingly restrictive REE production and export quotas, along with more stringent environmental legislation has caused a number of Chinese producers to close down, reduce production, or consolidate with other producers. In 2010, the Chinese government reduced its export quota (the limit set annually by the Chinese government on a company’s exports of REEs out of China) by 40%. This reduction, together with concordant trader speculation, led to rising export premiums, which in turn led to price increases of over 1000% for some LREEs.

An intense period of exploration for REEs during the 2000s led to the initiation of over 300 rare earth projects with varying degrees of viability. Estimated growth in REE demand over the next five years will only support between six and eight new producers. Developing a metallurgical flow sheet (a design plan for processing a material, specifically showing how material is moved around a processing plant from stage to stage) is paramount to a project’s success; project size has become less important. A number of rare earth exploration companies have affiliated themselves with specialist chemical or processing companies to provide assistance when developing their metallurgical flow sheet. As the REE market has matured, the ability to extract and process ore is now more important, and projects with established metallurgy have found it easier to gain financing.

The supply of rare earth elements in 2013 will continue to be dominated by China, although production in the rest of the world is expected to increase. New producers such as Lynas Corp. in Australia and Malaysia and SARECO in Kazakhstan have entered production, and existing producer Molycorp is scheduled to continue to ramp up production. Non-Chinese supply is forecast to reach 24,000t REO in 2013, which, although dwarfed by forecast Chinese production of 105,000t REO, is the highest production of REEs outside of China since the 1990s.

Along with primary mine production, rare earths can be sourced from recycling of materials. Research into recycling appliances containing REEs, including hard disk drives, fluorescent lamps, and NiMH batteries, is on-going. In 2011, Rhodia, a member of the Solvay Group, announced a partnership with materials technology group Umicore, to research recycling REEs from spent fluorescent lamps. In 2012, the company began a new initiative to recycle several hundred tonnes of linear and compact fluorescent lamps a year (2). Recycling of “new scrap” produced during the production process for NdFeB magnets has been widespread for some years now, to increase the efficiency of REE consumption. To date, however, there is no commercial recycling of “old scrap” NdFeB magnets to recover REEs; research into a cost-effective collection and processing scheme is on-going.

The reliance on Chinese production has led to reports highlighting the finite nature of Chinese REE resources, suggesting that current levels of supply may not be sustainable for an extended period. The life-of-mine at some deposits in Jiangxi province have been estimated at less than 15 years, and ore grades at Baiyun Obo operated by China’s largest REE producer Baotao Steel Rare Earth Group Hi-Tech Co. are reported to be declining. Extensive exploration within China, however, has identified a further 3.2Mt REO in Fujian province and 0.6Mt REO in Jiangxi province; furthermore, reserves in Guangxi province have been increased to 6.7Mt REO. Though grades at Bayun Obo are reported to be declining, the deposit has a reserve estimate of 28.8Mt REO, enough to sustain mining at current production rates for over 400 years.

In recent years, the rare earths elements have been defined in studies by the British Geological Survey (3), the European Commission (4) and National Research Council (5) to be amongst the group of critical elements. With production becoming increasingly geographically widespread and research into recycling and more efficient consumption underway, the criticality of REEs is expected to be reduced in the years to 2020, although China will maintain its position as the main producing and consuming nation.

References

1. R. L. Rudnick, S Gao (2003). Composition of the Continental Crust, in The Crust (ed. R. L. Rudnick) Volume 3, pages 1-64, Elsevier-Pergamon, Oxford.

2. Rhodia (Solvay Group) presentation, 8th International Rare Earths Conference, Hong Kong, 2012.

3. British Geological Survey, Rare Earth Elements, 2011, see www.bgs.ac.uk/downloads/start.cfm?id=1638.

4. Critical Raw Materials for the EU, Report of the Ad-hoc Working Group on defining critical raw materials, see http://ec.europa.eu/enterprise/policies/raw-materials/files/docs/report-b_en.pdf.

5. Committee on Critical Mineral Impacts of the U.S. Economy, Committee on Earth Resources, National Research Council, Minerals, Critical Minerals, and the U.S. Economy, National Academies Press, 2008.

DAVID MERRIMAN

Roskill Information Services Ltd., 54 Russell Road, London, SW19 1QL, UK E-mail: [email protected]

This article is based on a presentation by David Merriman at the ECG 2013 Distinguished Guest Lecture and Symposium held in the Science Room at Burlington House on Wednesday, March 20th 2013.

An intense period of exploration for REEs during the 2000s led to the initiation of over 300 rare earth projects with varying degrees of viability. Estimated growth in REE demand over the next five years will only support between six and eight new producers. Developing a metallurgical flow sheet (a design plan for processing a material, specifically showing how material is moved around a processing plant from stage to stage) is paramount to a project’s success; project size has become less important. A number of rare earth exploration companies have affiliated themselves with specialist chemical or processing companies to provide assistance when developing their metallurgical flow sheet. As the REE market has matured, the ability to extract and process ore is now more important, and projects with established metallurgy have found it easier to gain financing.

The supply of rare earth elements in 2013 will continue to be dominated by China, although production in the rest of the world is expected to increase. New producers such as Lynas Corp. in Australia and Malaysia and SARECO in Kazakhstan have entered production, and existing producer Molycorp is scheduled to continue to ramp up production. Non-Chinese supply is forecast to reach 24,000t REO in 2013, which, although dwarfed by forecast Chinese production of 105,000t REO, is the highest production of REEs outside of China since the 1990s.

Along with primary mine production, rare earths can be sourced from recycling of materials. Research into recycling appliances containing REEs, including hard disk drives, fluorescent lamps, and NiMH batteries, is on-going. In 2011, Rhodia, a member of the Solvay Group, announced a partnership with materials technology group Umicore, to research recycling REEs from spent fluorescent lamps. In 2012, the company began a new initiative to recycle several hundred tonnes of linear and compact fluorescent lamps a year (2). Recycling of “new scrap” produced during the production process for NdFeB magnets has been widespread for some years now, to increase the efficiency of REE consumption. To date, however, there is no commercial recycling of “old scrap” NdFeB magnets to recover REEs; research into a cost-effective collection and processing scheme is on-going.

The reliance on Chinese production has led to reports highlighting the finite nature of Chinese REE resources, suggesting that current levels of supply may not be sustainable for an extended period. The life-of-mine at some deposits in Jiangxi province have been estimated at less than 15 years, and ore grades at Baiyun Obo operated by China’s largest REE producer Baotao Steel Rare Earth Group Hi-Tech Co. are reported to be declining. Extensive exploration within China, however, has identified a further 3.2Mt REO in Fujian province and 0.6Mt REO in Jiangxi province; furthermore, reserves in Guangxi province have been increased to 6.7Mt REO. Though grades at Bayun Obo are reported to be declining, the deposit has a reserve estimate of 28.8Mt REO, enough to sustain mining at current production rates for over 400 years.

In recent years, the rare earths elements have been defined in studies by the British Geological Survey (3), the European Commission (4) and National Research Council (5) to be amongst the group of critical elements. With production becoming increasingly geographically widespread and research into recycling and more efficient consumption underway, the criticality of REEs is expected to be reduced in the years to 2020, although China will maintain its position as the main producing and consuming nation.

References

1. R. L. Rudnick, S Gao (2003). Composition of the Continental Crust, in The Crust (ed. R. L. Rudnick) Volume 3, pages 1-64, Elsevier-Pergamon, Oxford.

2. Rhodia (Solvay Group) presentation, 8th International Rare Earths Conference, Hong Kong, 2012.

3. British Geological Survey, Rare Earth Elements, 2011, see www.bgs.ac.uk/downloads/start.cfm?id=1638.

4. Critical Raw Materials for the EU, Report of the Ad-hoc Working Group on defining critical raw materials, see http://ec.europa.eu/enterprise/policies/raw-materials/files/docs/report-b_en.pdf.

5. Committee on Critical Mineral Impacts of the U.S. Economy, Committee on Earth Resources, National Research Council, Minerals, Critical Minerals, and the U.S. Economy, National Academies Press, 2008.

DAVID MERRIMAN

Roskill Information Services Ltd., 54 Russell Road, London, SW19 1QL, UK E-mail: [email protected]

This article is based on a presentation by David Merriman at the ECG 2013 Distinguished Guest Lecture and Symposium held in the Science Room at Burlington House on Wednesday, March 20th 2013.

Royal Society of Chemistry Environmental Chemistry Group

Burlington House

Piccadilly London W1J 0BA |

|

© COPYRIGHT 2022. ALL RIGHTS RESERVED.

Website by L Newsome

|